法律更新

Adjudication under Construction Industry Payment and Adjudication Act 2012 (“CIPAA”) is a temporary means of resolving payment disputes in the construction industry. Nevertheless, an adjudication decision is binding on parties until it is set aside or the dispute is finally resolved. Thus, it is possible and indeed an option for the successful party to an adjudication to commence winding up proceedings based on an adjudication decision under CIPAA.

The successful party in an adjudication may enforce an adjudication decision by applying to the High Court for an order to enforce the same pursuant to s. 28 of CIPAA. Once an order to enforce is obtained, s. 28(3) provides that the order may be executed in accordance with the same rules on execution of the orders or judgment of the High Court. This however is not compulsory for the purpose of commencing winding-up proceedings.

The Court of Appeal in the case of Likas Bay Precinct v. Bina Puri [2019] 3 MLJ 244, held that there is no requirement for the successful party in an adjudication to register the adjudication decision with the High Court under s. 28 of CIPAA before issuing a statutory notice to wind up. According to the Court of Appeal, winding up proceedings may be premised on an adjudication decision since it “evinces the fact that the amount stated therein is due and owing”. Thus, the successful party may commence winding up proceedings based on an adjudication decision without first obtaining an order to enforce the same under s. 28 of CIPAA.

In Likas Bay Precinct v. Bina Puri, the Court of Appeal held that the winding-up petition was not premature despite the adjudication decision not having first been registered under s. 28 of CIPAA. Having that said, the Court of Appeal noted that there was no application made for the adjudication decision to be set aside. In cases where there is an ongoing setting aside application, the Courts may take the view that the adjudicated amount in the adjudication decision is disputed (see: Visi Nusajaya v. Elite Alliance Engineering [2019] 1 LNS 945).

If you have any enquiries regarding the above or CIPAA, please do not hesitate to get in touch with our team.

| Lam Ko Luen Partner [email protected] |

Jeremy Ooi Associate [email protected] |

The Federal Court in the case of Jack-in Pile (M) Sdn Bhd v. Bauer (Malaysia) Sdn Bhd has confirmed that the Construction Industry Payment & Adjudication Act 2012 (“CIPAA”) does not apply to construction contracts entered into before the coming into force of the Act, i.e. 15.4.2014.

Flowing from this, the Federal Court held that the entire adjudication proceedings from which the court action originated, including the adjudication decision “are rendered void”. Consequently, the Federal Court held that the adjudication decision in those proceedings ought to be set aside.

The Federal Court’s decision represents a complete reversal of the earlier position in UDA Holdings Bhd v Bisraya Construction Sdn Bhd [2015] 11 MLJ 499 where it was held that CIPAA may apply retrospectively to pre-CIPAA contracts save where expressly excluded under the Act.

For more information on the above or CIPAA, you may contact:

Lam Ko Luen Victoria Loi Jeremy Ooi

Partner Partner Associate

[email protected] [email protected] jeremyooijr@shooklin.com.my

Bursa Malaysia Berhad (“Bursa Malaysia” or the “Exchange”) has, on 26 September 2019, issued a consultation paper seeking public feedback on the proposed amendments to the Main and ACE Market Listing Requirements (collectively “Listing Requirements”) in light of the government’s call under the National Anti-Corruption Plan (2019-2023). In that connection, Bursa Malaysia seeks the views and comments from the public in relation to the following two areas namely anti-corruption and whistle-blowing measures, as well as digitalisation of corporate exercises, which is explained in further detail below.

PART 1: STRENGTHENING THE GOVERNANCE OF LISTED ISSUERS TO PREVENT CORRUPTION, MISCONDUCT AND FRAUD

The Malaysian government has taken a strict stance against combating corruption and this is evident with the introduction of Section 17A of the Malaysian Anti-Corruption Commission Act 2009 (“MACC Act”) which takes effect on 1 June 2020 and has far-reaching implications to directors and corporations.

In this regard, Bursa Malaysia proposes to mandate a listed issuer to ensure that its board of directors does the following in order to promote a better governance culture and ethical behaviour across all levels of the listed issuer which is necessary towards sustainability of the listed issuer’s business in the long term:

(i) establish and maintain policies and procedures on anti-corruption that is guided by the Guidelines on Adequate Procedures (“GAP”) issued pursuant to Section 17A(5) of the MACC Act, or any other recognised framework which is similar to, or more stringent than the GAP (e.g. the Corporate Integrity System Malaysia or the ISO 37001 – anti-bribery management systems) and whistle-blowing;

(ii) conduct annual review of such policies and procedures, and publish them on the listed issuer’s website; and

(iii) include corruption risk in its annual risk assessment framework.

PART 2: PROMOTING OPERATIONAL EFFICIENCY AND EFFICACY THROUGH DIGITISING CORPORATE EXERCISES

Currently, securities holders subscribe for their rights shares or excess rights shares, convert their convertible securities into shares, or elect to participate in a DRS, manually. This would generally entail the completion and signing of the hard copies of the relevant forms, preparing the requisite payment in the form of a banker’s draft, cashier order, money order or postal order and the submission of the completed forms and requisite payment to the listed issuer’s share registrar personally either by hand, post or courier.

With innovations and advancements in technology, Bursa Malaysia believes that it is timely to modernise the current manual method through digitisation of some steps and accordingly, Bursa Malaysia proposes to require listed issuers to offer an option (in addition to the manual method) for its securities holders to perform the (i) subscription and payment for rights issue; (ii) conversion and payment for convertible securities; and (iii) election to participate in a dividend reinvestment scheme, electronically, either by way of an internet-based facility made available to securities holders, the use of automated teller machines or any other electronic mode as may be prescribed by Bursa Malaysia (eCorporate Exercise).

Additionally, Bursa Malaysia proposes to require a listed issuer to include (a) procedures for electronic conversion, in the notice of conversion or exercise of convertible securities; and (b) procedures for completing the election notice to participate in a DRS electronically, in the statement accompanying the election notice in the relevant notice or statement.

The consultation paper and the proposed amendments in Annexures A and B are available for download at Bursa Malaysia’s website (http://www.bursamalaysia.com/market/regulation/rules/public-consultation). Interested parties are invited to submit their comments and feedback to Bursa Malaysia by 25 October 2019 in the template table of comments prepared by Bursa Malaysia, either via (i) Email: [email protected]; (ii) Facsimile: +603 2732 0065; or (iii) Mail: Regulatory Policy & Advisory, Bursa Malaysia Securities Berhad, 9th Floor Exchange Square, Bukit Kewangan, 50200 Kuala Lumpur.

If you have any queries arising from the above developments, please do not hesitate to get in touch with our team:

| Ivan Ho Yue Chan

Partner

|

Karen Kaur

Partner

|

On 26.8.2019, the Federal Court heard, and allowed, the appeal of Affin Bank Berhad regarding when a bankruptcy order may be annulled. The issue of the ability of a debtor to pay his debts was considered as it was contended by the debtor that his ability to pay his debts had arisen subsequent to the bankruptcy order made, which led to the Courts below allowing the annulment of his bankruptcy.

In its decision, the Federal Court held that the ability of a debtor to pay his debts must relate to his ability to pay his debts as they became due, as at the date of the hearing of the creditor’s petition (commercial solvency). The fact that there may be circumstances subsequent to the bankruptcy order or that there are assets which may (but have not been) realised (balance sheet solvency) would not be sufficient to show ability to pay debts.

The Federal Court appeal was conducted by our Ms Yoong Sin Min and Ms Sharon Lim.

For further information, you may contact:

| Yoong Sin Min

Partner |

Sharon Lim

Senior Associate |

On 1 August 2019, the Federal Court in Martego Sdn Bhd v Arkitek Meor & Chew Sdn Bhd, (Civil Appeal Nos. 02(f)-2-01/2018(W) and 02(f)-3-01/2018(W)) has confirmed inter alia that the Construction Industry Payment & Adjudication Act 2012 (“CIPAA”) applies to interim and final payment disputes, thereby affirming the majority decision of the Court of Appeal ([2018] 4 MLJ 496).

Martego originated from an adjudication pursuant to CIPAA, initiated by consultant architects against the employer of a condominium project, for professional fees of RM599,500, after the contract had been terminated. In his adjudication decision, the adjudicator awarded the consultant architects a sum of RM258,550.

Subsequently, the employer applied to the High Court under s. 15 of CIPAA ([2017] 1 CLJ 101) to set aside the adjudication decision on the basis that, inter alia, CIPAA has no application in respect of architectural fees. The High Court dismissed the said application, holding that (i) an architect’s fees in respect of a construction contract are claimable under CIPAA and (ii) besides arbitration under the Architect’s Act 1967, CIPAA would be an additional mode of dispute resolution in respect of an architect’s fees, though only the former is final and binding.

On appeal, the majority of the Court of Appeal upheld the High Court’s decision. In the majority judgment, David Wong JCA (as his Lordship then was) held that it does not matter whether the payment claims were interim or final, or claims made after unilateral or mutual termination as long as they relate to a construction contract defined in s. 4 of CIPAA. Hamid Sultan JCA dissented and held that it was wrong to construe CIPAA to apply to claims for final payment when the mischief of the Act was intended to cure timely payment for work related to progress payments.

The employer appealed further to the Federal Court. The Federal Court, affirming the majority judgment of the Court of Appeal, unanimously held that there is no reason to confine the applicability of CIPAA to “interim claims” only. The Court stated that so long as there is a sum payable under a construction contract for work done and as long as the party remains unpaid, the claim can still be brought against the other party through CIPAA. The Court also confirmed that adjudication under CIPAA exists separately from arbitration (where provided for) and there was no question about one prevailing over the other.

Martego is a landmark decision by the Federal Court that has reinforced the position of CIPAA as a comprehensive albeit temporary avenue for the speedy resolution of payment disputes in construction contracts.

For more information about CIPAA, please contact our Mr Lam Ko Luen or Ms Victoria Loi.

| Lam Ko Luen

Partner

|

Victoria Loi

Partner

|

On 10.4.2019, the historic 9-member panel of Judges which was convened for the first time in such a large number to hear a constitutional reference of issues, delivered its judgment on whether legislative provisions which allowed the rulings of the Shariah Advisory Council (“the SAC”) are unconstitutional. The Judges included the Chief Justice of Malaysia, the President of the Court of Appeal, the Chief Judge of the High Court of Malaya, and the Chief Judge of the High Court of Borneo.

The constitutional reference arose in an action involving Kuwait Finance House (Malaysia) Berhad (“KFH”) and its customer, JRI Resources Sdn Bhd (“JRI”).

Shook Lin and Bok acted for KFH in the Federal Court reference hearing, through Ms Yoong Sin Min, Mr Samuel Tan and Mr Sanjiv Naddan.

A dispute had arisen as to whether a certain clause in the Ijarah agreements entered between KFH and JRI was shariah-compliant. The High Court referred the said clause to the Shariah Advisory Council (“SAC”) pursuant to Section 56 of the Central Bank of Malaysia Act 2009 (“the CMSA”) to obtain a ruling as to whether such clause/transaction was valid under Shariah law.

On 30.6.2016, the SAC (after having considered the written submissions of Islamic law experts who represented KFH and JRI respectively) issued its ruling.

The ruling was referred to the High Court, which then set the action down for trial. JRI, however, filed an application to refer questions to the Federal Court concerning the constitutionality of Sections 56 & 57 of the Central Bank of Malaysia Act 2009 (“the CBMA”) (“the Impugned Provisions“) and were permitted to do so.

The Federal Court thus sat on 28.8.2018 to hear the constitutional reference, with a 9-member panel of Judges being convened for the first time. Judgment was then reserved.

Due to the far-reaching consequences of the decision of the Federal Court, the Association of Islamic Banking Institutions of Malaysia and Bank Negara Malaysia had applied, and were allowed, to intervene and participate in the proceedings.

The main issues concerned whether the Impugned Provisions had the effect of vesting judicial power in the SAC and are therefore unconstitutional and void for contravening the Federal Constitution. The contention, in brief, was that s.56 of the CBMA (which requires the court to take into consideration a SAC ruling or to refer a question on Islamic law to the SAC), as well as s. 57 of the CBMA (which provides that any SAC ruling shall be binding on the court), have effectively usurped the Court’s judicial power to hear expert evidence itself to determine whether an Islamic banking transaction was shariah-compliant. KFH posed arguments to the contrary.

On 10.4.2019, the 9-member panel of Federal Court Judges held, by a majority of 5 to 4, that the Impugned Provisions are valid and constitutional. The majority Judges held, inter alia, that the role of the SAC did not usurp the powers of the Court as the SAC only ascertained the shariah law applicable to any Islamic banking transaction, with the final determination of the dispute still within the jurisdiction of the Civil Court. It was held that the SAC provided certainty to Islamic banking business. The minority Judges, which included the Chief Justice and the Chief Judges of Malaya and Borneo, however, expressed the view that the Impugned Provisions were unconstitutional as it effectively resulted in the SAC usurping an aspect of the judicial function of the Court. The dissenting Judges held that the separation of powers (between the legislative and judicial arms of the Government) must be strictly upheld.

| Yoong Sin Min

Partner

|

Chan Kok Keong

Partner

|

Samuel Tan

Partner

|

| We are delighted to share this triumph with our clients, who have entrusted us to chart the course and solve the complications.

We were awarded the ALB Litigation Law Firm of the Year 2019 at the prestigious Asian Legal Business Malaysia Law Awards on 28.3.2019! We thank you for your trust and support. We will continue to do what we do best, deliver excellent work and results. If you have any queries, please do not hesitate to get in touch with our team.

|

| Yoong Sin Min

Partner

|

Romesh Abraham

Partner |

| Lam Ko Luen

Partner

|

Chan Kok Keong

Partner |

| Section 241 of the Companies Act 2016 (“CA 2016”) has come into force on 15 March 2019.

With the coming into force of this section, any qualified person who wishes to act as a company secretary is now required to register with the Registrar of Companies (“Registrar”) irrespective of his or her professional background.

In line with the implementation of this section, the Companies Commission of Malaysia has introduced the Companies (Practising Certificate for Secretaries) Regulations 2019 and the Guidelines Relating to Practising Certificate for Secretaries under Section 241 of the Companies Act 2016 which serve to outline the parameters of the registration procedures as well as the duties and responsibilities of a company secretary.

Pursuant to the CA 2016 and the abovementioned regulations and guidelines, the Registrar will issue a practising certificate to an applicant upon being satisfied that all requirements have been complied with and the applicant is fit and proper to be registered, and enter the particulars of the applicant in the register of secretaries.

The CA 2016 also provides a transitional period whereby existing company secretaries may continue to act as secretary and they have a period of 12 months from the coming into force of Section 241 to register.

All applications for practicing certificates must be made online through https://esecretary.ssm.com.my |

If you have any queries arising from the above developments, please do not hesitate to get in touch with our team.

| Jalalullail Othman

Partner

|

Ivan Ho Yue Chan

Partner |

Khong Mei Lin

Partner |

Our firm recently hosted a 17-member delegation from the Zhuhai Lawyers Association. The delegation was led by the President of the Zhuhai Lawyers Association, Mr Tian Xue Dong and included committee members of the Association, all of whom are managing partners or senior partners of their respective firms. Both our guests and our partners engaged in fruitful discussions on the legal practice in Zhuhai and Kuala Lumpur. We hope to see more collaboration between our firm and our guests in the near future. Our firm wish to thank the Malaysian China Legal Cooperation Society for arranging this courtesy visit and making this event a success.

Securities Commission Public Consultation Papers: (A) Proposed Regulatory Framework for the Issuance of Digital Assets through Initial Coin Offerings (ICOs) and (B) Property Crowdfunding

The Securities Commission (“SC”) has, on 6 March 2019, published two consultation papers calling for feedback from the public on the framework to be used for ICOs and property crowdfunding. We set out brief details below.

A. PUBLIC CONSULTATION PAPER IN RESPECT OF A PROPOSED REGULATORY FRAMEWORK FOR THE ISSUANCE OF DIGITAL ASSETS THROUGH ICOs

ICOs are an alternative fundraising avenue that leverage distributed ledger technology including blockchain. In an ICO, an issuer who is typically an early-stage venture, creates and issues its own digital assets in exchange for established digital currency or fiat currency. The proceeds from the ICO are then purportedly used to build and develop its venture. The digital asset received by the investors is often representative of their interests, rights or benefits in the ICO issuer or the product or services of the ICO issuer. Examples of such rights and returns could include rights to monetary returns, projected returns from trading, access to facilities or discount entitlement on products.

This consultation paper sets out some background as to the nature of digital assets as well the risks involved in investing in such digital assets. It then proceeds to focus on the proposed regulatory framework for the issuance of digital assets through ICOs taking into account the needs of the industry on the one hand and investor protection on the other.

A two-pronged regulatory approach has been proposed by the SC, i.e.

- an authorisation for the offering / issuance of the ICO; and

- the registration of a disclosure document (“Whitepaper”) which complies with minimum requirements set by the SC.

In relation to (a), the SC proposes undertaking an assessment of the ICO by applying specific criteria for the assessment of the ICO as well as imposing eligibility criteria on the issuer of the ICO. Accordingly, the consultation paper discusses, among other things, issues such as the fit and properness of an ICO issuer and its directors and management and the digital value proposition of the ICO’s underlying business / project. It is proposed that a potential ICO issuer must be a locally incorporated company which has its main business within Malaysia and has a minimum paid up capital of RM500,000. In the initial phase of the ICO framework, the SC also proposes that the issuer should not be a public listed company. Other proposals include limiting the amount of investment that can be raised through an ICO, requiring at least 50% of the proceeds of an ICO to be utilised in Malaysia (or if the ICO is asset-backed, ensuring that at least 50% of the assets are based in Malaysia) and restricting the withdrawal or utilisation of investors’ monies by the ICO issuer to milestones disclosed in the Whitepaper.

The SC also proposes that an ICO issuer be required to approach a third party to agree to “host” the ICO and assess its Whitepaper prior to it submitting a formal application to the SC. It is proposed that the third party “host” be a recognised market operator or other person recognised by the SC as having the necessary skills and expertise.

In relation to (b), the SC proposes that any offering of an ICO must be accompanied by a Whitepaper which must be submitted for registration by the SC. Such Whitepaper will need to meet the disclosure requirements stipulated by the SC. In deciding whether or not to register a Whitepaper, the SC may take into consideration the pre-approval evaluation and assessment carried out by the third party service provider, or recognised market operator (as discussed above).

B. PUBLIC CONSULTATION PAPER IN RESPECT OF A PROPOSED REGULATORY FRAMEWORK FOR PROPERTY CROWDFUNDING

Property crowdfunding aims to provide an alternative source of financing, particularly tailored to first-time homebuyers. It is intended to enable a first-time homebuyer to access funding to purchase his or her first property. At the same time, it will enable investors to access a new type of investment product.

As a concept, property crowdfunding refers to a form of online fundraising that envisages a homebuyer obtaining funds to pay for the purchase price of a property through investments from a relatively large number of investors via an online platform publicising and facilitating such transactions. Investors who are platform members can browse through a list of properties offered on the platform to find opportunities that meet their investment criteria (for example, the location, property type, entry level, estimated returns and the background of the proposed homebuyer). The investors put in their investment sum, which is then held by the platform operator until the fundraising target is achieved.

This consultation paper starts by laying down the basic mechanism of a property crowdfunding scheme and the relevant risks to be considered. It then proposes several regulatory requirements to be imposed on the property crowdfunding scheme and its participants to mitigate risks involved with such a scheme, such as –

- imposing requirements on platform operators- such as criteria to qualify as a platform operator, obligations of a platform operator and permissible and non-permissible activities of a platform operator;

- imposing requirements on homebuyers, such as criteria for homebuyers who can seek funding on the platform, funding limits and obligations of homebuyers; and

- specifying the criteria of the type of properties that can be hosted on the platform.

The SC envisages that a property crowdfunding scheme must have in place an avenue for investors to exit their investment at the end of the scheme’s tenor. Some exit options include –

- sale of the property at a price determined by an independent valuer whereby the returns to the investors, if any, will be the difference between their initial investment and the amount of money raised from the sale of the property;

- a platform operator providing a warehousing facility, where a homebuyer may sell the property to the platform operator based on a market value determined by an independent valuer; or

- having in place an underwriting agreement with a bank to provide a loan to pay off the amount due to investors.

Finally, the consultation paper proposes allowing secondary trading of investment notes relating to a property crowdfunding scheme on its platform to enable investors to sell their investment notes and cash out their position without the need to wait for the scheme’s tenor to end.

Both abovementioned consultation papers are available at the SC website (https://www.sc.com.my/regulation/consultation-papers). Written comments from the public in relation to the consultation papers are to be submitted to [email protected] by 29th March 2019.

If you have any queries arising from the above developments, please do not hesitate to get in touch with our team.

| Ivan Ho Yue Chan

Partner

|

Tan Gian Chung

Partner |

Karen Kaur

Partner |

Two recent developments have impacted the Malaysian regulatory landscape in relation to digital assets, digital exchanges and their operators.

Digital Currencies and Digital Tokens are Securities

Firstly, the Capital Markets and Services (Prescription of Securities) (Digital Currency and Digital Token) Order 2019, which came into force on 15 January 2019, provides that digital currencies and digital tokens which fulfil certain specific features (and are neither issued nor guaranteed by any government body or central bank) are prescribed as securities.

This prescription of digital currencies and digital tokens as securities is significant as it subjects them to the application of the provisions of the Malaysian Capital Markets and Services Act, 2007 (“CMSA”). This in turn, affects how such digital currencies and digital tokens can be offered in Malaysia.

By prescribing certain digital currencies and digital tokens as securities, any person who wishes to make available, offer for subscription or purchase, or issue an invitation to subscribe for or purchase the same will be required to seek the approval of the Securities Commission (“SC”) under the CMSA and register a disclosure document. It is anticipated that the SC will issue, by the first quarter of 2019, the relevant regulatory requirements for the offering of digital currencies and digital tokens (e.g. initial coin offerings) and the trading of such digital assets.

Another significant consequence of such prescription is that persons who carry on a business of dealing in digital currencies and digital tokens would fall under the licensing regime under the CMSA.

Guidelines on Recognized Markets

The second development was the revision by the SC of its Guidelines on Recognized Markets on 31 January 2019 (the “Guidelines”). The revision, among other things, introduces new requirements for electronic platforms that facilitate the trading of digital currencies and digital tokens, and follows the coming into force of the Capital Markets and Services (Prescription of Securities) (Digital Currency and Digital Token) Order 2019.

Under the Guidelines, any person who is interested in operating a digital asset platform is required to apply to the SC to be registered as a recognized market operator.

If you have any queries arising from the above developments, please do not hesitate to get in touch with our team.

| Ivan Ho Yue Chan

Partner

|

Tan Gian Chung

Partner |

Karen Kaur

Partner |

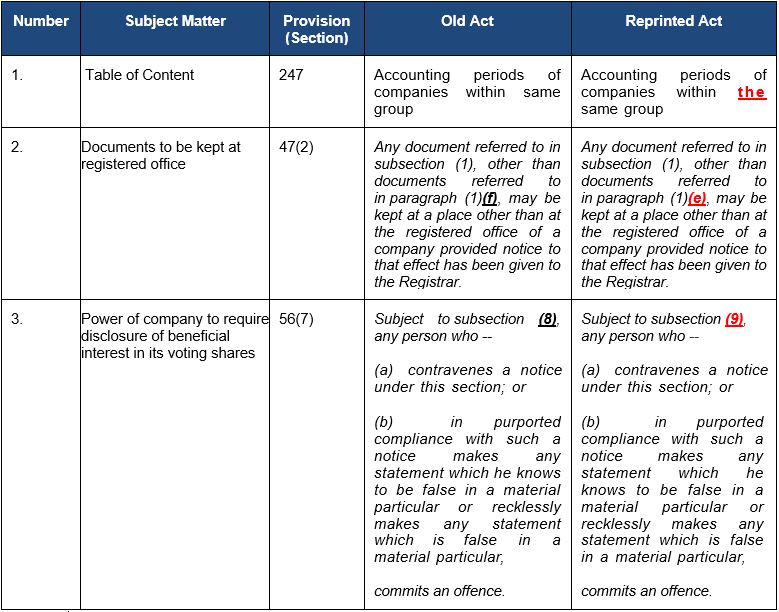

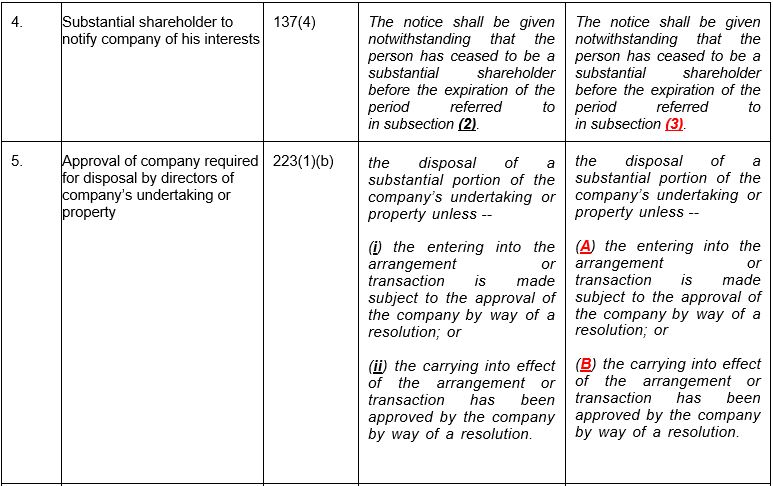

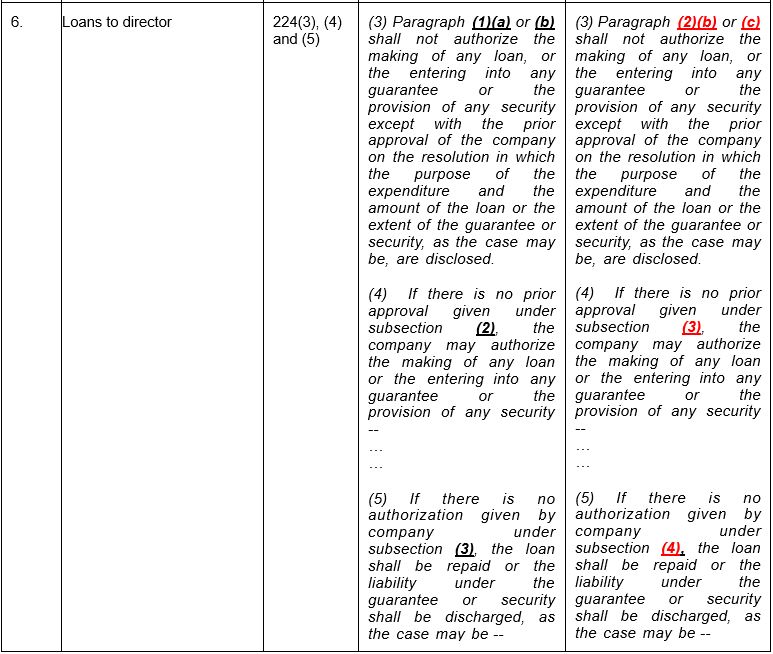

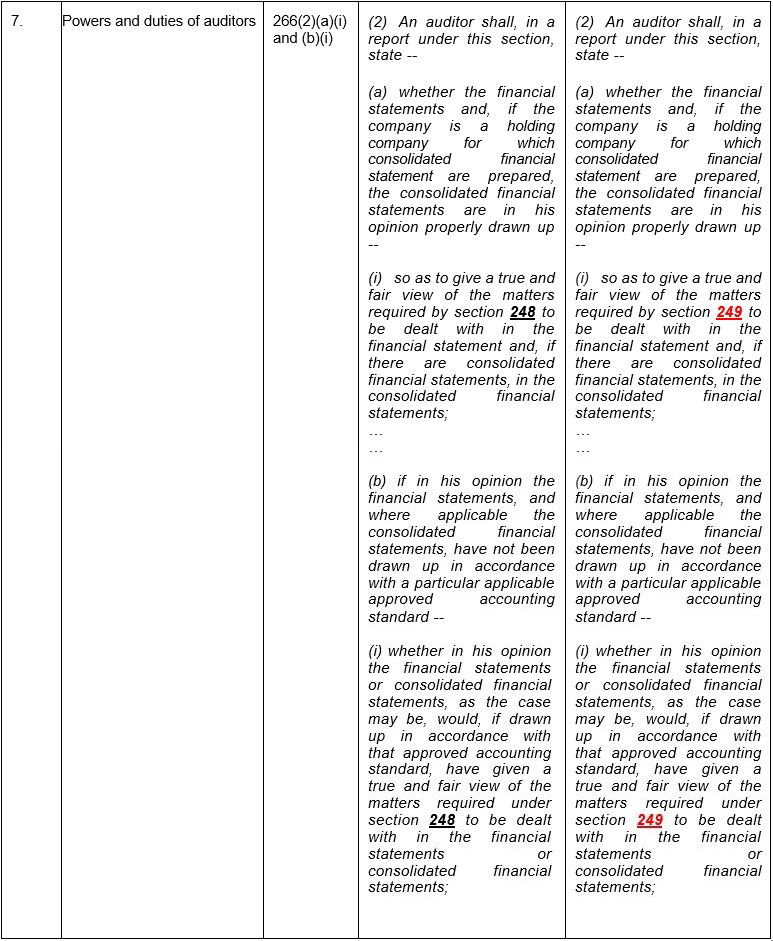

The Companies Commission of Malaysia announced on its website that the Companies Act 2016 (“Act”) has been reprinted as at 1 November 2018, and the same will be the authoritative text of the Act. Minor revisions have been made to the Act by the Commissioner of Law Revision pursuant to Section 14(1) of the Revision of Laws Act 1968, and for ease of reference, these changes are summarised in the following table:

If you have any queries arising from the above developments, please do not hesitate to get in touch with our team.

| Ivan Ho Yue Chan

Partner

|

Jalalullail Othman

Partner |

Khong Mei Lin

Partner |

A recent Court of Appeal decision sent waves of consternation amongst financial institutions, when the Court decided that a bank was time-barred from pursuing any further applications to fix a fresh auction date, on the basis that limitation had set in more than 12 years AFTER the date of the Order for Sale.

In the case of RHB Bank Berhad v Dato’ Haji Muhammad bin Hamzah, the bank had attempted numerous times to realise land charged to it through court-conducted auctions but the auctions were all unsuccessful due to lack of bidders.

The chargor then applied in the charge action for an order that the bank could no longer file any further application for a new auction date to be fixed, on the basis that limitation had set in as more than 12 years after the Order for Sale had lapsed.

The Court of Appeal, on 5.7.2018, agreed with the chargor and relied on sections 21(1) and 6(3) of the Limitation Act 1953 in so deciding.

This is the first time the Court has declared that the limitation period would preclude further applications AFTER the Order for Sale had been granted.

Shook Lin and Bok took over the matter and on 28.11.2018, obtained leave to appeal from the Federal Court.

In view of the recent wave of decisions from the Court of Appeal where financial institutions have been found to be time-barred in their realisation of charge actions, the Federal Court has agreed to hear this appeal together with an earlier appeal pending before it, i.e., the case of CIMB Bank Berhad v Sivadevi A/P Sivalingam.

Keep an eye on this space for further developments.

If you have any queries arising from the above developments, please do not hesitate to get in touch with our team.

| Yoong Sin Min Partner[email protected] |

Heng Chia Leng Senior Associate[email protected] |

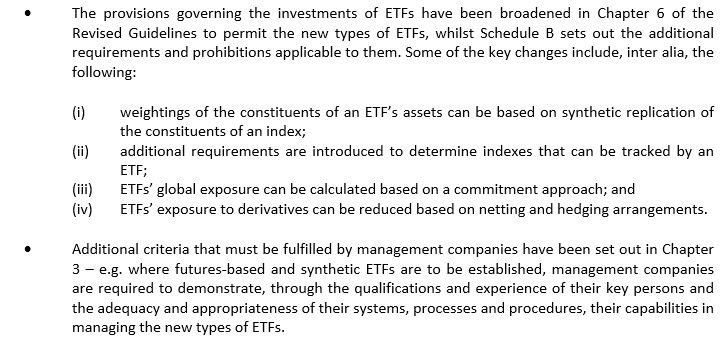

Guidelines on Exchange Traded Funds

On 26 November 2018, the Securities Commission (“SC”) announced a revision to the Guidelines on Exchange Traded Funds (“Revised Guidelines”) which will pave the way for the issuance of a more diversified range of exchange traded funds (“ETFs”) in Malaysia. The Revised Guidelines, which will come into effect on 2 January 2019 (“Effective Date”), allow asset managers to offer a wider array of ETFs which includes futures-based ETFs (including leveraged and inverse ETFs), synthetic ETFs and commodity ETFs. A number of key changes have been made in the Revised Guidelines, in particular:-

In addition to the above, other changes include (i) requirements to allow the establishment of multiple classes of units within an ETF; (ii) requirements to allow for both cash or in-kind creations and redemptions, or a combination of cash and in-kind creations and redemptions; (iii) a new requirement to allow Islamic ETFs to participate in Islamic Securities Selling and Buying – Negotiated Transaction (“ISSBNT”) activities.

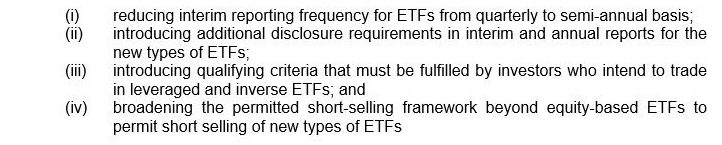

Main Market Listing Requirements & Bursa Malaysia Securities Berhad Rules and Directives

In tandem with the Revised Guidelines, on 7 December 2018, Bursa Malaysia Securities Berhad (“Bursa”) announced enhancements to the ETF framework by way of amendments to the Main Market Listing Requirements (“MMLR”) and Bursa Malaysia Securities Berhad Rules and Directives (“Bursa Rules & Directives”). These amendments will similarly come into operation on the Effective Date.

The amendments to the MMLR and Bursa Rules & Directives aim to facilitate the trading of the new types of ETFs on Bursa. Some key changes include:

Given the above developments and revisions and the limited time before these changes will come into effect, relevant parties (e.g. asset managers, management companies, advisors and trustees) are advised to promptly ascertain how these changes may affect their businesses to ensure full compliance with the relevant regulatory requirements prior to the Effective Date.

If you have any queries arising from the above developments, please do not hesitate to get in touch with our team.

Ivan Ho Yue Chan Jalalullail Othman Khong Mei Lin

Partner Partner Partner

[email protected] [email protected] meilinkhong@shooklin.com.my